Today’s drop in inflation potentially sets the stage for less tightening - or even easing - in the medium term, leading to a resurgence in inflation later in the cycle, eventually requiring a significant re-tightening of monetary conditions. Even if today’s fall in consumer-price inflation means we are over the peak, and it continues to slow, we are still probably only in the first act of a three act play.

The 1970s are an imperfect analogy, but they have one crucial aspect in common with today: the monetization of large fiscal deficits. Runaway inflation is almost always preceded by large government borrowing financed by the central bank.

Both the late 1960s and the last few years saw rising fiscal deficits facilitated by a central bank that thought it had more room to ease than it really did, as was the case in the late 1960s and early 1970s; or one that decided to ignore rising inflation altogether, as the Fed did with its recent maximum-employment/average-inflation-targeting framework.

Once the conditions for high inflation are there, the economy is at the mercy of “events”, whether that be the Arab Oil Embargo in the early 1970s, or the pandemic and the Ukraine war in the current period.

We are now in Act I, where inflation is high and rising. We will soon enter Act II, where a respite in inflation hoodwinks the Fed into believing it can take its foot off the tightening pedal prematurely. This sets the stage for Act III, where price growth stops falling, and takes off again, this time making new highs.

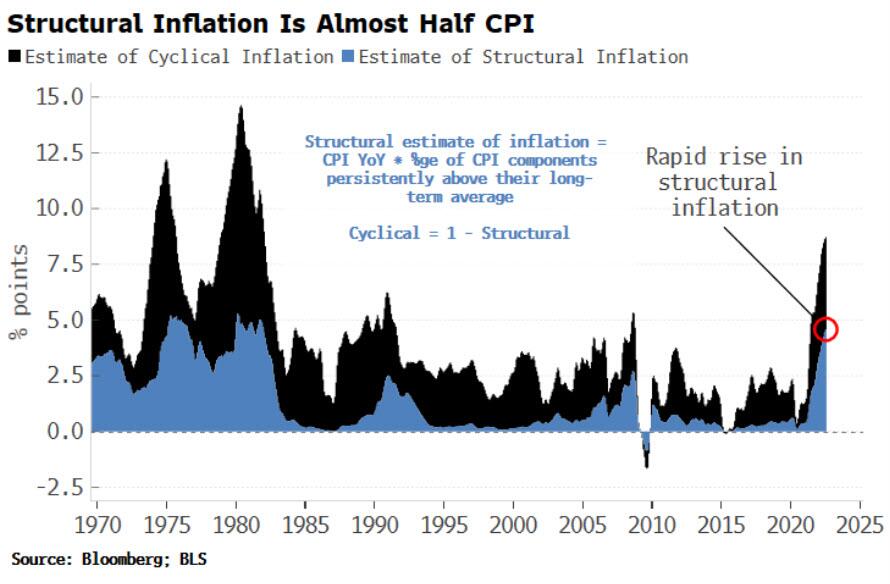

But what’s maybe happening under the surface here? A way to think about this is to quantitatively break up inflation into cyclical and structural components.

Cyclical price pressures should soon start to ease, taking the headline number down. But, as the chart below shows, the estimate for structural inflation is very high, making up almost half the headline number.

If almost half of current inflation proves harder to shake, the cyclical-driven fall in the headline number would only be cosmetically positive. Once the cyclical components start contributing positively again, they would reinforce the stickier, structural inflation, potentially leading CPI to new highs.

This would be Act III, and we know from the Volcker era how that has to end.